The 2026 income tax scale, applicable to income earned in 2025, was revalued by 0.9% under the 2026 Finance Act, enacted on 19 February 2026. This is a more modest increase than last year's 1.8% in 2025, and well below the 4.8% recorded in 2024, a signal that the government is tightening the indexation of the scale to strict inflation rather than pursuing a broader purchasing-power support policy. This article details the five brackets of the 2026 tax scale, the calculation method based on the family quotient, the tax relief mechanism for lower-income households, and corrective measures such as the surcharge on high incomes, which now affects a growing share of executives and business owners.

For companies managing the taxation of business travel and expense reimbursements, this scale also has indirect effects on compensation trade-offs and mobility policies. If you want to professionalise the management of your business trips alongside your tax obligations, you can request a Fairjungle demo.

How the progressive income tax scale works

The French income tax scale, or IRPP, is built on a principle of progressivity: each bracket of income is taxed at its own rate, from the lowest to the highest, much like a staircase where every step has its own price. Contrary to a widespread misconception, the marginal tax rate, that of the highest bracket your income reaches, never applies to your entire income, only to the portion that exceeds that bracket's threshold. A single taxpayer declaring 40,000 euros in net taxable income does not pay 30% on the whole amount: they pay 0% on the first 11,600 euros, 11% on the next bracket, and only 30% on the remainder.

To apply the scale, the tax authorities first divide your net taxable income by the number of shares in your tax household, known as the family quotient. A single person counts as one share, a married or civil-partnered couple as two shares, and each child adds an extra half-share for the first two, then a full share from the third child onward. The progressive scale is then applied to this income per share, and the result is multiplied by the number of shares to obtain the household's gross tax.

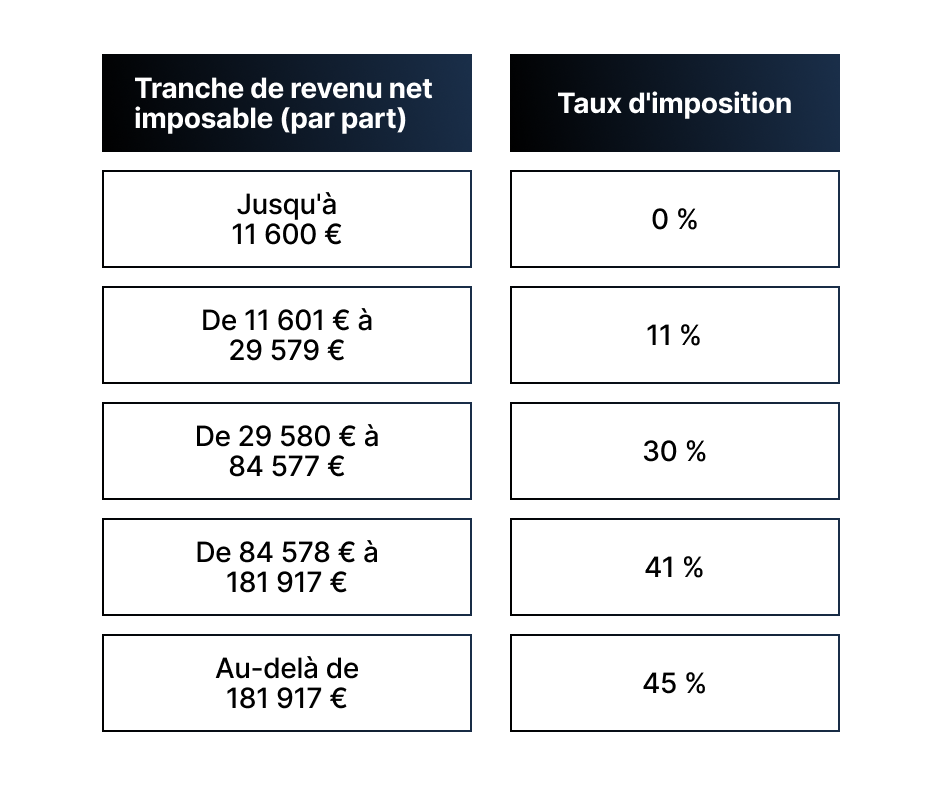

2026 tax scale: the five income brackets

Here is the 2026 income tax scale, applicable to 2025 income declared in spring 2026, per share of the family quotient.

Take the example of a single taxpayer, one share of the family quotient, with an annual net taxable income of 30,000 euros. The first 11,600 euros are not taxed. The next bracket, from 11,601 to 29,579 euros, or 17,979 euros, is taxed at 11%, roughly 1,978 euros. The remainder, from 29,580 to 30,000 euros, or 421 euros, is taxed at 30%, roughly 126 euros. The total comes to around 2,104 euros, an average rate of about 7% of net taxable income, far below the 30% marginal rate shown on their tax notice.

Family quotient and the cap on additional half-shares

The family quotient reduces the tax burden for households with children or dependants, but its benefit is not unlimited. For 2025 income, the tax reduction linked to each additional half-share is capped at 1,807 euros. In practice, if the theoretical benefit from additional shares exceeds this cap, the authorities recalculate the tax using the capped amount rather than the full quotient. This mechanism mainly affects higher-income households with several children, for whom the gain from the family quotient would otherwise be disproportionate.

Take a married couple with two children, three shares of the family quotient, with a net taxable income of 60,000 euros. Income per share is 20,000 euros. After applying the scale per share and multiplying by three, the gross tax is compared with what the same couple would have paid without the children's half-shares, plus the 1,807-euro cap per half-share. If the actual benefit exceeds this cap, the capped amount prevails. This mechanism, often misunderstood, explains why two households with identical income but different family composition can end up paying very similar amounts beyond a certain income level.

The tax relief (décote): a correction for lower-income households

The décote is a second mechanism that reduces, or even cancels, the gross tax for lower-income households, smoothing the entry into taxation to avoid a sharp threshold effect when leaving the 0% bracket. It applies automatically when the tax calculated after the scale remains below a certain threshold, which varies according to family situation. It can reduce the tax due by several hundred euros, and in some cases eliminate it entirely. On top of this, a non-collection rule applies: no payment is collected if the annual tax due is below 61 euros.

These two mechanisms combined explain an often-cited statistical paradox: roughly half of French tax households fall within the 11% marginal bracket, yet a significant share of them ultimately pay no income tax at all, once the décote and other corrections are applied.

The surcharge on high incomes, renewed for 2026

The differential contribution on high incomes, or CDHR, introduced under the 2025 Finance Act, has been renewed under the 2026 Finance Act. It aims to guarantee a minimum effective tax rate of 20% for the wealthiest households, adding to the existing exceptional contribution on high incomes. It applies to households whose reference tax income exceeds 250,000 euros for a single person, or 500,000 euros for a couple. When the combined amount of income tax and the existing surcharge remains below this 20% threshold of reference tax income, an additional contribution applies to close the gap.

This renewal for 2026 is an important signal for business owners and high-earning self-employed individuals, particularly those who receive a significant share of their compensation as dividends taxed under the progressive scale rather than the flat tax. The CDHR calculation adds to the usual trade-off between the 30% flat tax and opting for the progressive scale, a choice that must be reassessed each year based on the household's income structure.

How to calculate your 2026 tax step by step

Calculating your 2026 tax on 2025 income follows a well-defined multi-step method. Start by determining your net taxable income, meaning all your income after automatic deductions, notably the 10% flat-rate deduction for professional expenses on salaries, capped at 14,555 euros and with a floor of 509 euros per person. Then divide this income by the number of shares in your tax household to obtain income per share. Apply the progressive scale to this amount, bracket by bracket, to obtain the tax due per share. Finally, multiply this result by the number of shares to obtain the household's gross tax.

At this stage, several adjustments can still change the final amount: the cap on the family quotient if your household includes dependants, the décote if your income remains modest, then any tax reductions and credits you may be entitled to, such as donations, home employment, or rental investments. For the wealthiest households, the existing surcharge and the CDHR are finally added to the calculation. If you would rather avoid manual calculations, the tax authorities provide an official simulator on their website to precisely estimate your tax on 2025 income.

What actually changes compared with the 2025 scale

The main development in the 2026 tax scale lies less in its structure, unchanged with its usual five brackets, than in the scale of its revaluation. After 4.8% in 2024 and 1.8% in 2025, the 0.9% increase applied in 2026 marks a clear slowdown in the scale's indexation to inflation. For a taxpayer whose income grows at the same pace as inflation, the effect remains broadly neutral. But for households whose income stagnates or grows more slowly than prices, this weaker revaluation gradually pushes them into a higher bracket, a phenomenon tax specialists call fiscal drag, or bracket creep.

Another point of continuity worth noting: the CDHR, initially presented as a measure limited to 2024 and 2025 income, has indeed been renewed for 2026 income, confirming that it was not a one-off measure but a lasting tool in high-income taxation. For companies, these tax developments interact directly with compensation and expense reimbursement policy, particularly when employees have to weigh different compensation options linked to their travel. Our guide on business travel expense reimbursement details how to structure this process effectively.

The impact of the tax scale on corporate travel policy

The income tax scale does not directly determine corporate taxation, but it deeply influences the individual decisions employees and executives make regarding business expenses. An employee close to the 30% or 41% bracket threshold has a stronger tax incentive to optimise their actual expense deduction, including mileage allowances, a topic we cover in detail in our guide on the 2026 mileage scale. Similarly, trade-offs between benefits in kind, bonuses and travel expense reimbursements become more significant as an employee's marginal tax rate rises.

For a finance or HR department, understanding these tax mechanics helps refine the company's travel and reimbursement policy, taking into account not only the direct cost of travel but also its tax impact on employees. A well-built corporate travel policy incorporates these parameters to offer trade-offs that benefit both the company and its employees.

Centralising the tax and budget management of your travel

The 2026 tax scale is part of a broader set of rules, mileage scale, deduction caps, décote, family quotient, that make manual expense management increasingly complex for both companies and their employees. Centralising travel booking and tracking on a single platform provides a consolidated view of costs, secures compliance with internal policies, and considerably simplifies the production of documentation needed for everyone's tax returns.

This centralisation also has a direct impact on the finance department's budget planning, allowing it to anticipate the effect of tax changes on travel costs rather than discovering them after the fact. If you are preparing a consultation to structure your business travel programme, our guide on the travel agency request for proposal sets out the method to follow. And to see concretely how a next-generation business travel agency like Fairjungle simplifies this oversight, the simplest step is to book a demo.

In summary

The 2026 tax scale, applicable to 2025 income, keeps its five-bracket structure but was revalued by only 0.9%, a markedly slower pace than the previous two years. The calculation still relies on the family quotient, corrected by the cap on half-shares and the décote for lower-income households, while the differential contribution on high incomes, renewed this year, continues to target households with a reference tax income above 250,000 or 500,000 euros. Beyond individual tax compliance, these developments have concrete implications for corporate travel and reimbursement policy, an area where centralised management brings real added value.